- The Wealthy Prognosis

- Posts

- No Ragrets

No Ragrets

Dying with zero in more ways than one.

Howard & Peter

April 12, 2026

OUR ADDICTION TO PEARLS

We couldn’t capture all the great pearls of this book with just one blog. Though many of the lessons are intuitive, the manner in which the author illustrates them resonate so strongly with us. In this second blog, we want to review the few remaining topics. Some of them include areas that Peter and I have not given much conscious thought, despite having witnessed them in our own personal lives.

Perhaps the biggest lesson for us was that of charitable giving and inheritance. As we’re only in our 30s, the idea of donations on a grand scale, be it a cause or inheritance, has not really crossed our minds. We are still in the building phase of our lives. Of course, we always knew we’d build toward a financially secure future so that any future offspring would not need to take care of us in our decrepit age. Naturally, we’d want to also endow them with financial security as well. We wouldn’t want this generosity limited to just potential offspring but family and friends in general.

So then, where was the big breakthrough? The book points out that most people come into inheritance when their parents or loved ones pass. That is, people receive inheritances when they are well into their 60s or 70s these days. Traditional inheritance at that age provides little opportunity for meaningful experiences. Moreover, the person doing the giving cannot enjoy the fruits of their generosity. By giving or donating earlier in your life, your children or cause can enjoy the money while you’re still live. This will also be much more impactful in the moment rather than delaying any sort of benefit.

One example the author uses to really drive home this point is the fact that most people need their inheritance most in their late 20s or 30s. This age group faces significant financial challenges just newly burgeoning, with family planning and housing as the big ones. Early transfers of wealth are stupidly obvious with this logic, with virtually little downfall if executed thoughtfully. As discussed in the last blog, most people save up their retirements for potential medical expenditures. Many people never actually utilize the money in that way (i.e. pass away before actually spending it down). Even so, is it really worth it? Possibly, but in many circumstances not really.

If this reasoning weren’t enough, the author goes on to say that inheritances and wealth transfers are essentially large scale investments in your children. When raising children, you want to give them ample opportunities. Music lessons, sports, extracurriculars—you name it and many parents are happy to spend. After all, investing in children’s activities and cultivating their passions builds memories and has long-term positive outcomes. This logic should extend even into their adulthoods. The memory dividends once again are so worth it. Just as you can enjoy ballet lessons with your child, you can as easily cultivate invaluable memory dividends from them pursuing adult things (like grandchildren)!

This was perhaps the most impactful chapter for myself. I always considered myself lucky as my parents shouldered much of the financial burden of higher education. I only ever could see it from my perspective. Now, I understand just how meaningful it must have been (and still is) for them to see me with more flexibility in job opportunities, location, and life enjoyment. Had I walked away from all this schooling with the full burden of student debt, I would have felt much more trapped in selecting for jobs qualifying for PSLF (often restrictive in geography) and needing to penny pinch everyday. And in all likelihood, the money would instead still be sitting idle in my parents’ accounts untouched. They would’ve watched me struggle needlessly with less chance to spend time with or near them. What good is that?

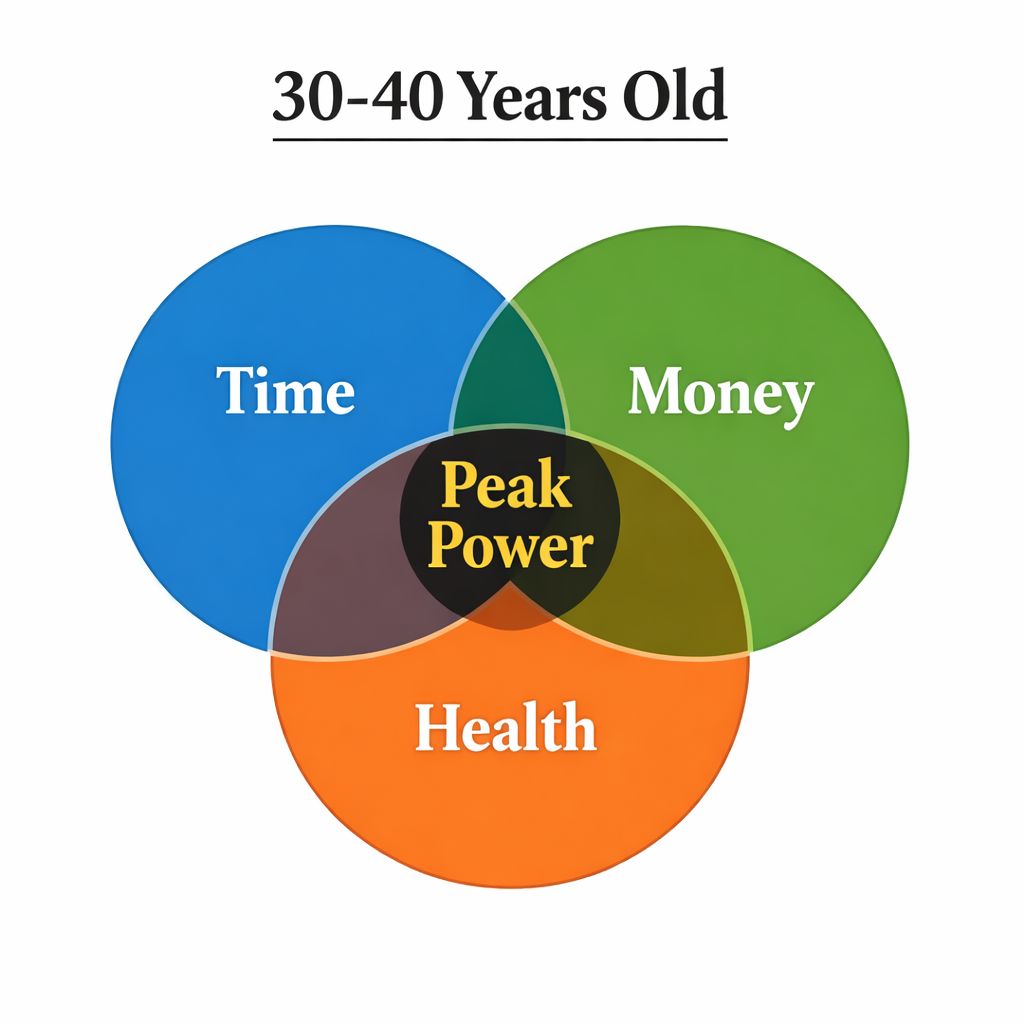

With this chapter over, we delved into the topic of resources. In this life, we have three resources: time, money, and health. Early on, we have abundant time and health, but less (or no) money. Later in life (60s-80s), we have more money and time (freed from the shackles of work), but declining health. It is somewhere between our 30s-40s that we have the best balance of all three resources. Peak power.

One perspective I haven’t taken regarding health is how it compounds negatively, just like how money may compound positively. For example, being 10 pounds overweight can easily snowball into bigger issues, such as decreased mobility due to joint pain, fatigue, and more resultant weight gain. Declining health drastically reduces life fulfillment, one that is always so apparent to us as healthcare workers.

I believe it was the Dalai Lama who made apparent to me one of the greatest ironies of life. He stated that people sacrifice health in the pursuit of money and in our old age, we will then trade money for health often out of necessity. In the end, we have only lost time and gained nothing. Perhaps it is no surprise then that the research supports spending money to free up time rather than material purchases. It is the acquisition of time to pursue other endeavors that bring us greatest satisfaction. Of course, money should also be spent primarily on meaningful experiences rather than “things.” Experiences, after all, are often constrained by the parameters of time and health.

Listening to this chapter was reminiscent of our trip to Japan in August 2025. We spent a pretty penny to stay in a ryokan in Hokkaido. For Peter, it financially did not make sense to pay such exorbitant dollars just to stay on a resort while traveling abroad. However, because of the unique opportunity of it being our first ryokan and being abroad with dear friends, we had no qualms about it. As we think about our parents and their advancing age, there is no price we wouldn’t pay to ensure their comfort and enjoyment.

This segues into the next big topic: delayed gratification. When is it worth endeavoring on an expensive experience versus delaying it? Perhaps in our youth, we can delay that dream trip to Mexico by a year in order to push our career one step further, as the benefit greatly outweighs the delay. However, when we are in our 60s or 70s, delaying that dream trip has a much higher chance of never actually coming to fruition. Maybe in our 20s, we can work hard so that we can go on multiple vacations in the subsequent years. But in our 70s, waiting until we’re 80 so we can go on two trips instead of one just doesn’t make sense. Similarly, one-time events or experiences also cannot be delayed, such as weddings, birthdays, and other celebrations. We use this chapter’s teachings to justify our FIRE mindset, despite the rest of the book (essentially) preaching balance.

I’ve rambled somberly about death in several past blogs, and I am glad the author also touches upon this topic. In fact, he writes that throughout our lifetimes, we each suffer innumerable “deaths.” More commonly, we refer to these as “chapters” of our lives. Still, we often think of them on the scale of years or big, sentinel events. If we view this logic through lens of raising children, it forces us to look more at the microscopic events happening around us. Children develop and change rapidly over the span of months! A child at 2 years of age will be dramatically different from when they’re 3 years old. As the adage goes, we can always make more money but we can never turn back time (or gain more health for that matter). It’s a resource we only have less of with each passing day.

Mindful use of our time in the pursuit of our happiness is correlated with higher life satisfaction. Though Peter enjoys a packed schedule and I do not, we are equally happy with our life trajectories. And because of this, we try not to let finances confine our choices as there is usually a budget version of everything if it would truly make us happy.

We’d say that the golden years are actually between 20-60, or 40 +/- 20 years. This aligns with our own goals to achieve FIRE sometime within our early to mid 40s to then work part-time for fulfillment. We’d then start spending down that nest egg on the super expensive stuff, like raising a family, home ownership, and eventual wealth giving. We’d also like to account for ways in which we can maximize enjoyment with potential children. That is, buying back time when or if we have children so that we can be more present parents. A prime example is housekeeping! Of course, filling their lives with experiences that we can share together can quickly become costly as well.

In his last few chapters, the author delves into the importance of not being complacent. For the time being, we think we are on a good trajectory. We spend fairly freely on the things that matter and have no alternative while saving aggressively where we can. Though our terminal degrees have traditionally conferred unshakeable job security, it becomes less certain each and every day with artificial intelligence. Who knows what the world and our careers will look like in 10 or 15 years?

Though I enjoy the current stability, Peter and I are wary of simply coasting. We are certainly not risk-seeking, but we do understand that our ability to bounce back should an unfavorable endeavor go awry is much higher when we are younger. It may also yield financial and psychological rewards (such as satisfaction or happiness), should we leap for opportunities. For the time being, no such opportunities have presented itself so we are staying put in our occupations. We’d be remiss, however, if we closed ourselves off to any opportunities whatsoever in the name of stability or due to risk avoidance.

As a financial guide, one may assume that the title refers to dying with zero dollars left. After a complete reading, we come to understand that it’s a guide on dying with zero regrets. The book’s goal is not to literally die with zero dollars, but to create a mindset shift. Even if we die with money remaining, the value comes from making conscious efforts to prioritize experiences throughout life. As Bill Perkins puts it, “the business of life is the acquisition of memories.”

XOXO,

Howard and Peter